First, I summarise the arguments of O’Brien.

According to O’Brien, the short recession beginning in August 1918 appears to have been the result of conversion from wartime to peacetime production, and only lasted 7 months (O’Brien 1997: 151).

The mildness of this recession and the mild deflation appear to have boosted business and consumer confidence (O’Brien 1997: 152).

The increased confidence, together with the pent up demand for consumption goods and capital goods, led in 1919 to a boom in residential construction, fixed investment and automobiles (O’Brien 1997: 152).

What set off the recession in 1920 was the following factors:

(1) early in 1920 there were declines in sales, particularly textile products and iron and steel;Thus a major part of the recession was a contraction in business investment and production to liquidate excess inventory.

(2) continued cuts to government spending and government purchases in 1919;

(3) exports declined by 20% between the 1st and 2nd quarters of 1920;

(4) the Federal Reserve raised discounts rates to 4.75% in late 1919, and then 6% in early 1920. The New York Federal Reserve even raised its discount rate to 7% on 1 June, 1920. This caused a contraction in business and consumer credit, and

(5) since many businesses had accumulated raw materials and intermediate goods in the expectation of further inflation, when the recession struck they suffered heavy losses and in order to reduce inventory they cut production sharply (O’Brien 1997: 152).

To this extent, 1920–1921 was somewhat like post-1945 “inventory” recessions, in which contractions were partly the result of previous and excessive inventory accumulation and then the subsequent liquidation of this stock (Sorkin 1997: 569).

Next, we turn to Samuelson. According to Samuelson (1943: 47–50), demobilisation was largely finished by the first half of 1919, and one year after the armistice of November 1918 4 million men had been discharged (Samuelson 1943: 47).

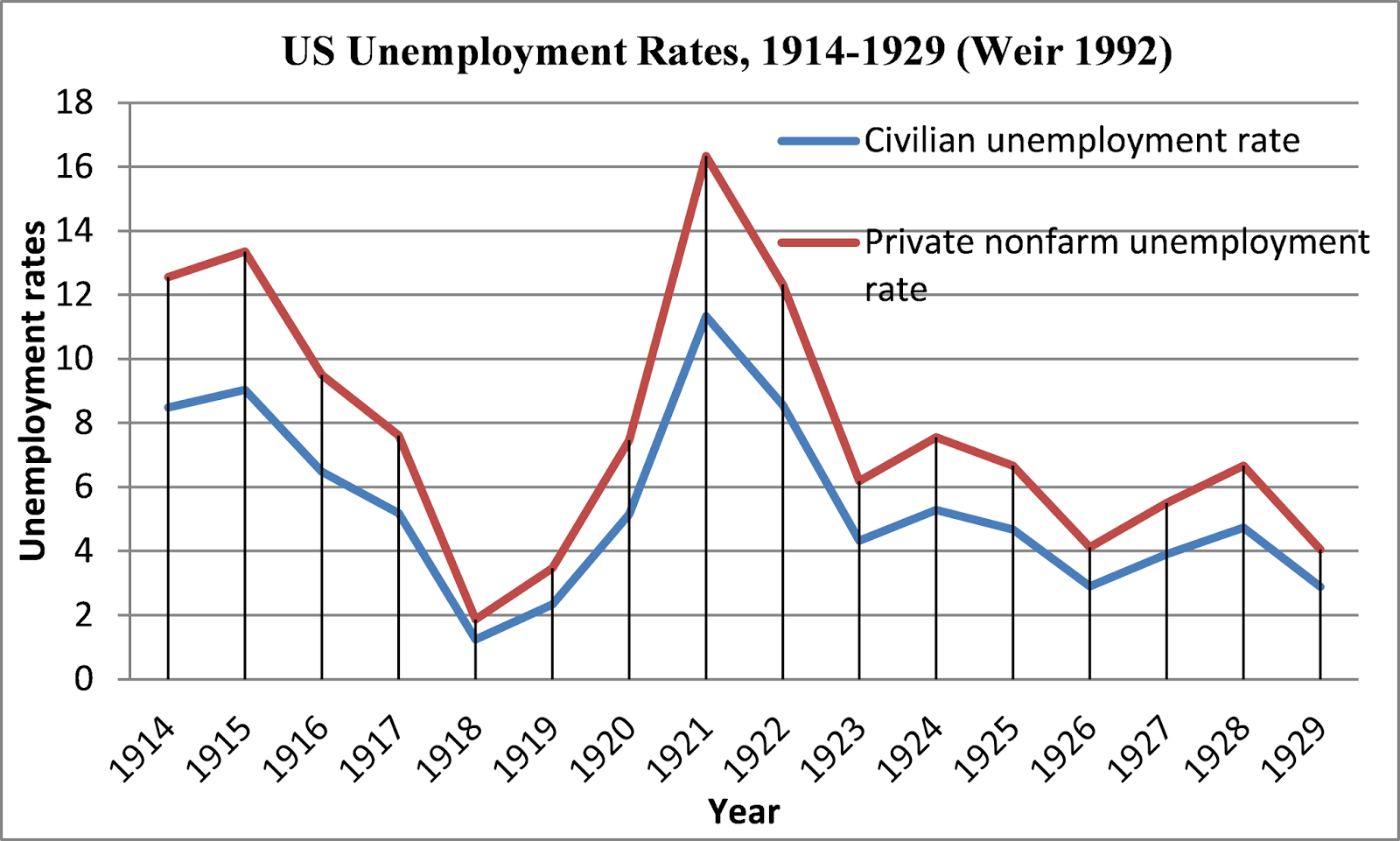

As an aside, we can note that unemployment was already rising in 1919, as can be seen in the graph below (from Weir’s [1992] unemployment estimates).

So the rise in unemployment in 1920 and 1921 came on top of the previous unemployment caused by demobilisation.

Samuelson (1943: 48–49) further argues that the boom of 1919 was very much dependent on continued government spending, even if that spending was falling.

Just as O’Brien, Samuelson emphasises the role of business confidence and inventory accumulation in 1919:

“Not knowing the troublesome times ahead, the private business community greeted peace with optimism. As the spring of 1919 wore on, sales increased in retail lines such as clothing for returning soldiers, household goods, etc. With the removal of price controls, the wholesale price index began to rise, in the end soaring from the final war level of around 200, on a prewar base, to almost 250. This set off a wave of inventory accumulation, or attempted accumulation, which formed a substantial fraction of total offsets to savings; and the paper increase in inventory values was considerably greater.So both O’Brien and Samuelson have a broadly similar story on the cause of the recession of 1920–1921.

From its nature this was an unhealthy base upon which to erect a boom. Price increases led to attempted inventory accumulation, further accentuating the price increases. But it was not enough for prices to stay at these abnormal levels; once they ceased to rise, or leveled off, the whole structure had to collapse.” (Samuelson 1943: 49).

Further research has explained the nature of the recession itself. It was an anomalous recession. Real output contraction only became severe after July 1920 (Vernon 1991: 573), and Vernon (1991: 575) points out that even the large rise in unemployment in 1920 is to be explained to some extent by the continued effects of the previous demobilisation and increased immigration in 1920 and 1921.

Romer (1988: 97–99) argues that total consumption from 1920 to 1921 actually increased, not fell, because, even though consumer expenditures on durable goods contracted, expenditures on nondurables and services increased to make up for the shortfall.

Finally, there is still disagreement about the depth of the recession.

Romer (1989) provided a new estimate for GNP declines from 1920 to 1921, as follows:

Year | GNP* | Growth RateThese estimates show a GNP contraction of only 3.47% from 1919 to 1921, a mild to moderate recession.

1914 | $414.599

1915 | $443.048 | 6.86%

1916 | $476.498 | 7.54%

1917 | $473.896 | -0.54%

1918 | $498.458 | 5.18%

1919 | $503.873 | 1.08%

1920 | $498.132 | -1.13%

1921 | $486.377 | -2.35%

1922 | $514.949 | 5.87%

1923 | $583.105 | 13.23%

* Billions of 1982 dollars

(Romer 1989: 23).

By contrast, Balke and Gordon (1989: 84–85) estimate a GNP decline of 5.58% from 1920–1921, a moderately bad recession.

On either of these estimates, however, the downturn of 1920 to 1921 was nothing like the Great Depression, and it still appears to be an anomaly.

Further Reading

“The US Recession of 1920–1921: Some Austrian Myths,” October 23, 2010.

“There was no US Recovery in 1921 under Austrian Trade Cycle Theory!,” June 25, 2011.

“The Depression of 1920–1921: An Austrian Myth,” December 9, 2011.

“A Video on the US Recession of 1920-1921: Debunking the Libertarian Narrative,” February 5, 2012.

“The Recovery from the US Recession of 1920–1921 and Open Market Operations,” October 4, 2012.

“Rothbard on the Recession of 1920–1921,” October 6, 2012.

“The Recession of 1920–1921 versus the Depression of 1929–1933,” February 2, 2014.

“Debt Deflation: 1920–1921 versus 1929–1933,” February 3, 2014.

“US Wages in 1920–1921,” February 10, 2014.

BIBLIOGRAPHY

Balke, N. S., and R. J. Gordon, 1989. “The Estimation of Prewar Gross National Product: Methodology and New Evidence,” Journal of Political Economy 97.1: 38–92.

O’Brien, Anthony Patrick. 1997. “Depression of 1920–1921,” in D. Glasner and T. F. Cooley (eds), Business Cycles and Depressions: An Encyclopedia. Garland Pub., New York. 151–154.

Romer, C. D. 1988. “World War I and the Postwar Depression: A Reinterpretation based on Alternative Estimates of GNP,” Journal of Monetary Economics 22.1: 91–115.

Romer, C. D. 1989. “The Prewar Business Cycle Reconsidered: New Estimates of Gross National Product, 1869–1908,” Journal of Political Economy 97.1: 1–37.

Samuelson, Paul A. 1943. “Full Employment after the War,” in Seymour E. Harris (ed.), Postwar Economic Problems, McGraw-Hill, New York and London. 27–53.

Sorkin, A. L. 1997. “Recessions after World War II,” in D. Glasner and T. F. Cooley (eds), Business Cycles and Depressions: An Encyclopedia. Garland Pub., New York. 566–569.

Vernon, J. R. 1991. “The 1920–21 Deflation: The Role of Aggregate Supply,” Economic Inquiry 29: 572–580.

Weir, D. R. 1992. “A Century of U.S. Unemployment, 1890–1990: Revised Estimates and Evidence for Stabilization,” Research in Economic History 14: 301–346.

The export collapse was actually relatively late; the import collapse came before that. There was a small import boom between the 1918-19 and 1920-21 recessions.

ReplyDeletehttp://research.stlouisfed.org/fred2/graph/?g=FqL